- Argentina(Español)

- Österreich (Deutsch)

- Belgium(English)

- Belgique (Français)

- België(Nederlands)

- Brasil (Português)

- Canada(English)

- Canada (Français)

- Chile(Español)

- China(Chinese)

- Colombia(Español)

- Czechia(Czech)

- Denmark(Danish)

- República dominicana(Español)

- France (Français)

- Deutschland (Deutsch)

- Hungary(Hungarian)

- Italia(Italiano)

- 日本(日本語)

- Kazakhstan(Kazakh)

- Kazakhstan(Russian)

- Luxembourg(Français)

- Mexico(Español)

- Maroc(Français)

- Nederland(Nederlands)

- Panamá(Español)

- Perú(Español)

- Poland(Polish)

- Portugal (Português)

- Puerto Rico(Español)

- Romania(Romanian)

- Slovakia(Slovak)

- España (Español)

- Taiwan(Chinese)

- Tunisie(Français)

- Turkey(Turkish)

- Ukraine(Ukrainian)

- United States(English)

- Uruguay(Español)

- Venezuela(Español)

Managing Complex and Disputed Insurance Claims

When the unexpected occurs, how does your business react? What steps are taken to mitigate further risk or potential losses? And when does somebody consider whether insurance might respond?

Most businesses invest significant time in the insurance buying process to analyse risks and consider risk transfer options.However, during a crisis, a business may find itself overwhelmed, or focused on the immediate response to the claim or loss. Insurance can either be forgotten or put on the shelf to be dealt with later. This is particularly true where the insurance claim is likely to be complex, financially significant, or both. These claims involve an increased burden on the business when managing the recovery, which can be seen as a distraction from the main effort of managing the loss.

As risks evolve, insurance policy response is tested against factual scenarios that are unchartered territory for insurers and policyholders. As society becomes more interconnected, regulated, and litigious, losses have the potential to be more frequent and severe. As such, the likelihood of your business needing to manage a complex insurance recovery is more likely than ever before.

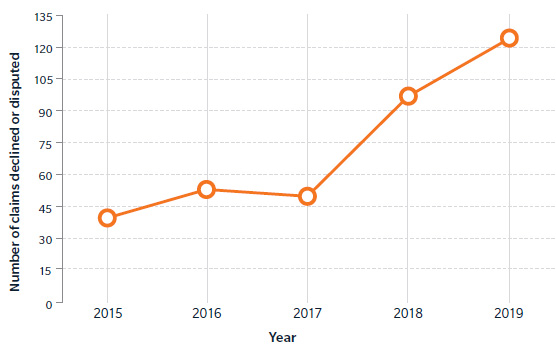

Additionally, the insurance industry continues to scrutinise claims, deploying significant legal resource to assist doing so. The number of declined or disputed claims continues to rise (see Figure 1), a trend we do not expect will change as the insurance market continues to transition.

Although no two claims are the same, certain strategies can help to maximise the outcome of claims in most circumstances.

In our guide, we give you practical tips that can help you to resolve complex and disputed recoveries. By collaborating with insurers and internal stakeholders, issues can be avoided or overcome,relationships preserved, and the real value of insurance can be realised.